pandas进行量化回测

神出鬼没,指的就是我! 人气:0下面文章描述可能比excel高级一点,距离backtrader这些框架又差一点。做最基础的测试可以,如果后期加入加仓功能,或者是止盈止损等功能,很不合适。只能做最简单的技术指标测试。

导包,常用包导入:

import os

import akshare as ak

import requests

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import talib as ta

%matplotlib inline

plt.style.use("ggplot")获取数据,本文使用akshare中债券数据为对象分析:

bond_zh_hs_daily_df = ak.bond_zh_hs_daily(symbol="sh010107")

添加指标:

def backtest_trend_strategy(ohlc: pd.DataFrame, fast_period: int = 50, slow_period: int = 200, threshold: float = 1.0) -> pd.DataFrame: """封装向量化回测的逻辑""" # 计算指标 ohlc["fast_ema"] = talib.EMA(ohlc.close, fast_period) ohlc["slow_ema"] = talib.EMA(ohlc.close, slow_period) ohlc["pct_diff"] = (ohlc["fast_ema"] / ohlc["slow_ema"] - 1) * 100 # 生成信号,1表示做多,-1表示做空,0表示空仓 ohlc["signal"] = np.where(ohlc["pct_diff"] > threshold, 1, 0) ohlc["signal"] = np.where(ohlc["pct_diff"] < -threshold, -1, ohlc["signal"]) # 计算策略收益率 ohlc["returns"] = np.log(ohlc["close"] / ohlc["close"].shift(1)) ohlc["strategy"] = ohlc["signal"].shift(1) * ohlc["returns"] ohlc["strategy_returns"] = ohlc["strategy"].cumsum() return ohlc

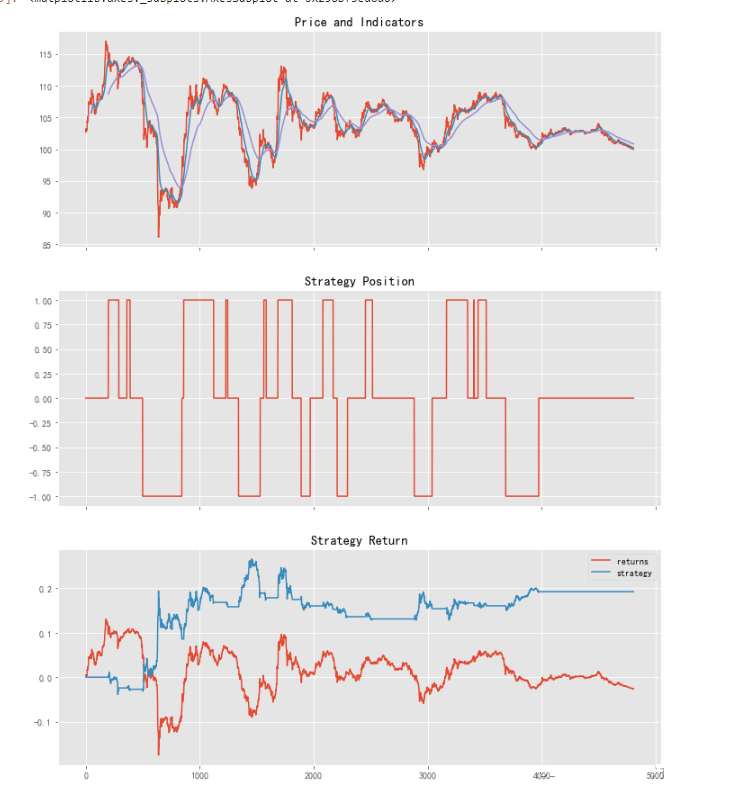

运行策略,并绘制图片:

data = strategy1(data)

fig, ax = plt.subplots(nrows=3, ncols=1, figsize=(12, 15), sharex=True)

ax[0].plot(data.index, data["close"])

ax[0].plot(data.index, data["fast_ema"])

ax[0].plot(data.index, data["slow_ema"])

ax[0].set_title("Price and Indicators")

ax[1].plot(data.index, data["signal"])

ax[1].set_title("Strategy Position")

data[["returns", "strategy"]].cumsum().plot(ax=ax[2], title="Strategy Return")

参数优化:

# 选择核心参数和扫描区间,其它参数保持不变

fast_period_rng = np.arange(5, 101, 5)

total_return = []

for fast_period in fast_period_rng:

ohlc = data.filter(["open", "high", "low", "close"])

res = backtest_trend_strategy(ohlc, fast_period, 200, 1.0)

total_return.append(res["strategy_returns"].iloc[-1])

# 散点图:策略收益率 vs 快速均线回溯期

fig, ax = plt.subplots(figsize=(12, 7))

ax.plot(fast_period_rng, total_return, "r-o", markersize=10)

ax.set_title("Strategy Return vs Fast period")

ax.set_xlabel("fast_period")

ax.set_ylabel("return(%)")加载全部内容